It’s the end of the beginning for the economy, not the other way around

The economic expansion and stock market run-up have been going on for a decade, and a case of the jitters seems to be spreading. How long can this go on? Is the end around the corner?

After years of quiet, the stock market suddenly became volatile again last March. Volatility is a sign of uncertainty and often presages a decline. Stock prices are high relative to earnings and dividends, which often precedes a fall.

{mosads}Short-term interest rates have risen, and long-term rates and short-term rates are nearly the same. An inverted yield curve, when short-term rates are higher than long-term rates, is one of the most reliable warning signs of a recession.

The unemployment rate is down to 3.9 percent, a level that historically has only happened at business cycle peaks — that were soon followed by troughs. House prices and credit are up too, as they were at recent peaks.

Larry Summers, writing in his May Financial Times column, warned that “secular stagnation” could still be right around the corner. In his view, the economy is only growing because of the fiscal stimulus of trillion-dollar deficits and extraordinarily loose monetary policy, and by a stock market bubble itself fueled by monetary policy.

“What we are seeing is the achievement of fairly ordinary growth with extraordinary policy and financial conditions. Something similar took place in the years before the Great Recession.”

A small downturn would then turn in to a rout as “the fiscal cannon has already been fired… leaving policymakers short on ammunition,” he stated.

Martin Feldstein, writing in the Wall Street Journal, warned similarly, “Year after year, the stock market has roared ahead, driven by the Federal Reserve’s excessively easy monetary policy. The result is a fragile financial situation— and potentially a steep drop somewhere up ahead.”

And the economic boom is similarly perilous: “Easy monetary policy has produced an overly tight labor market that is beginning to push up inflation. …[that] will cause long-term rates to rise even before that faster inflation occurs.”

Is it time to batten the hatches and worry? Well, yes, always worry, but I think these predictions of imminent disaster are overblown.

When the unemployment rate hits 4 percent, it is a good sign that the economy has moved from “demand” to “supply.” The U.S. economy can no longer produce more by simply matching people looking for work with idle machines.

To grow now, we need more people or better machines and businesses. We need to bring people into the workforce who aren’t now even looking for work, or we need higher productivity.

A supply economy responds to incentives, not to stimulus. Taxes matter now not so much by how much money people keep, but by the incentives or disincentives they give to work, save and invest, i.e., marginal tax rates.

The recent tax cut was not so important for “putting money in pockets” and greater stimulus, as it is for raising the incentive to invest at the margin. The administration’s regulatory reform effort likewise boosts the economy by giving greater incentive to invest.

But these are first steps. Our tax code is still agonizingly complex and full of disincentives to work, save and invest. The regulatory reform program must be seen to last and not quickly reversed with the next president’s pen and phone.

Our social programs also badly need reform. Many people do not work, or work more, because they lose more than a dollar’s benefits, or access to their home or health care, if they work.

More growth from more demand is over, but supply-side growth can continue for years. If we are to grow now, it will be from better supply and policy focused on incentives.

In my view, Summers overstates fiscal stimulus. Back in the 2008 recession and the big debates over President Obama’s stimulus plans, fiscal stimulus advocates were usually careful to say that stimulus works only when there are substantial numbers of unemployed people, and when interest rates cannot move, being stuck at the zero bound.

Summers seems to have forgotten those crucial caveats. Large deficits in good times are not good policy, but because they run up the debt, not because they stimulate.

In my view, both authors — and the very common views they represent — vastly overstate the Federal Reserve’s power. There is very little evidence that quantitative easing did anything at all and certainly not anything that lasted a long time.

The 10-year bond rate has been on a steady downward trend for the last 20 years, and there is no visible correlation between Fed bond buying and interest rates or inflation.

The Fed has for 10 years been taking in reserves and paying more on them than banks can get elsewhere. A central bank pushing down rates would have been doing the opposite.

There is no theory or evidence that the Fed has an outsized influence on asset prices. Stocks are rising in this expansion at the same rate they have risen in previous expansions — and much slower than the late 1990s boom.

The price/dividend ratio is high — but, accounting for low interest rates, it is exactly where it has been in previous expansions. Risk premiums are always low in late expansions, when the economy is doing well and people are willing to take risks.

There is no theory other than repeated assertion by which the level of interest rates or bond buying has anything to do with the risk premium in stocks.

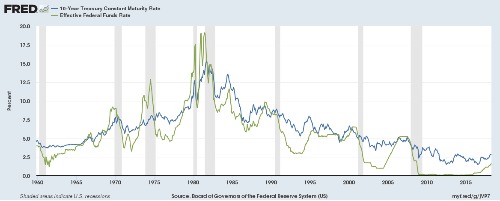

The graph shows the 10-year government bond rate and the overnight federal funds rate, which the Fed controls. Notice how an “inverted” spread — when the funds rate is higher than the 10-year rate — is one of the most reliable indicators of a recession to come.

Notice that the yield spread is tightening now. So should we worry? Well, notice also the many times when the yield spread tightened — and then sat there for many years of growth. The late 1960s, the late 1980s and the late 1990s are good examples.

A tight yield spread is one sign the economy has moved from demand- to supply-side growth, but not that the party is over. The party is over in long-term bonds.

A large spread between long- and short-term yields does reliably signal better returns in long bonds, as risk premiums are high in times of depressed demand. That risk premium, like other premiums, is at its natural business-cycle low.

Here is the unemployment rate. Yes, below-4-percent unemployment was last seen in 2000, just before the first of two recessions. Gloom and doom? Well, notice again the late 1960s, the late 1980s and to some extent the late 1990s. When the economy turns from “demand” to “supply,” it can trundle along a long time with steady low unemployment and inflation.

So I see no evidence that our growth is supported by unusual stimulus. The economy has finally recovered from the 2008 recession. Demand is over. Further growth depends on supply — larger productivity or labor force, and supply depends on incentives. It is the end of the beginning, not the beginning of the end.

And we need luck. We will grow until something happens. Recessions don’t happen on their own, and a longer expansion does not make a recession more probable. A recession needs a spark, something to go wrong.

Feldstein is right, a panic monetary tightening from the Fed could be that spark, as it has so many times before. A new financial crisis somewhere in the world — perhaps a government debt crisis — could be that spark. A war or a trade war could be that spark. “Don’t screw up” is policy advice often overlooked in the quest for dramatic action.

One thing we know for sure — recessions are unpredictable. If we knew for sure a recession would happen in the near future, then it would already have happened today. If we knew stocks would go down tomorrow, they would have already gone down today.

If companies knew business would be bad next year, they would stop investing, and business would be bad today. So take all predictions with that grain of salt — but examine hard the logic behind them.

John H. Cochrane is a senior fellow of the Hoover Institution at Stanford University, specializing in financial economics and macroeconomics, and an adjunct scholar of the Cato Institute. He is a frequent contributor to The Wall Street Journal and Bloomberg.

Copyright 2023 Nexstar Media Inc. All rights reserved. This material may not be published, broadcast, rewritten, or redistributed.