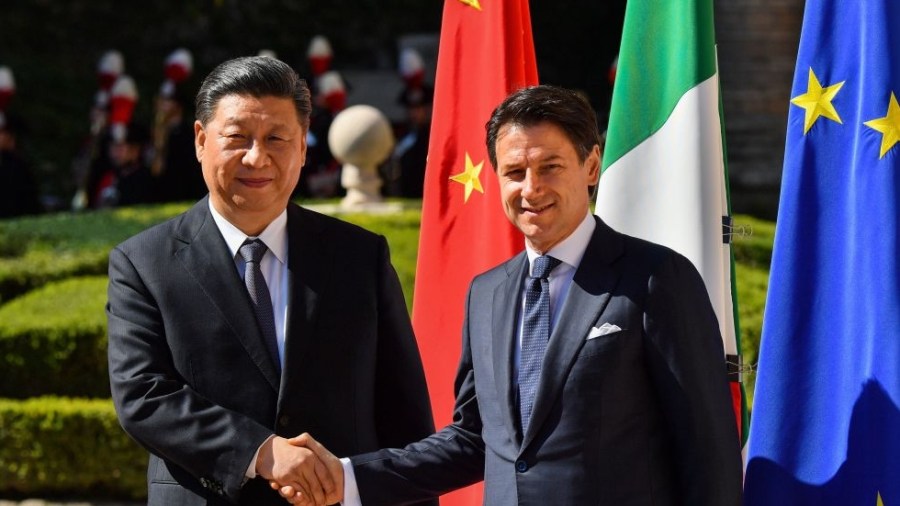

The Italian fanfare over Chinese President Xi Jinping’s recent visit illustrates how anxious Prime Minister Giuseppe Conte is to bolster the Italian economy by welcoming China’s Belt and Road Initiative (BRI) into Italy.

He expects these Chinese commitments to translate into real investment that will generate jobs and boost exports to China. Importantly, by restoring Italy’s ancient role as the gateway to and from Asia, Chinese investment can improve transport within Italy and on to Europe, adding to Italy’s services economy as well.

{mosads}Italian and Chinese entities signed several agreements committing to future financing, trade, joint construction projects and cooperation in international fora.

Briefly, an Italian lender will be able to raise funds in China by issuing yuan-denominated bonds to Chinese investors while the Bank of China will lend to Italian companies. E-commerce ties will be deepened, and tourism promoted.

But the heart of the understandings is Chinese investment in Italian industry, oil and gas, transport and others. All of this is enveloped in broad language that refers to past Europe-China agreements and joint support for international initiatives such as the Paris Agreement on climate change.

Nonetheless, despite the appearance of openness, trade and investment facilitation and reinforcement of past agreements, Italy’s European partners, as well as U.S. officials have deep reservations.

European leaders are currently adopting EU-wide investment screening procedures they feel are needed to protect European national security. The Italy-China agreement highlights deeper cooperation in science and technology, more collaboration between scientific personnel and institutes as well as startups.

While there is a nod to respecting intellectual property rights, there is nothing explicit regarding technology transfer or how Italy would protect the intellectual property of its European partners. Furthermore, EU members have not been able to effectively enforce their own agreements.

While European leaders are loath to admit this, they likely fear that they will not be able to control or even know the details of Chinese involvement in the Italian economy.

Other important details are missing or not revealed. What will be the financial agreements that will underpin BRI investments in Italian ports, railroads, roads and related services? Asian countries have already raised fears that Chinese investments lead to high debt and loss of domestic control.

Sri Lanka had to cede control of a port to the Chinese because it could not service the related debt. Malaysia and other countries have cancelled projects that closer examination revealed added more to debt than to real productive capacity to service that debt.

Italy’s debt levels are already very high and further increases due to Chinese BRI activities would add to market nervousness.

The lack of transparency overall will be a persistent problem as there is no central repository or system-wide control in China over the terms of BRI-related lending and investment. Chinese entities undertaking these investments do not publicize the details of the agreements and most likely do not share these details with a central government entity in Beijing.

There is no explicit reference to Italian or Chinese participants in these projects being required to provide information on the terms of these agreements to government entities that might be able to raise red flags early enough to fend off or amend problematic agreements.

These same concerns are front and center for U.S. officials. Potential Chinese involvement in Italian communications networks will raise fears regarding network security in Europe and then in the United States, given the broad and deep ties between U.S. and European systems.

Rapid increases in Italian debt to Chinese entities will raise the risk of a future eurozone debt crisis. An Italian debt crisis will be much worse than Greece’s financial crisis and much more difficult for the eurozone to handle.

{mossecondads}Italy’s size and core historical role in the European Union and eurozone monetary union mean a financial crisis would significantly stress the union. This would test other EU countries’ willingness to bail out a partner, particularly if the beneficiary of that bailout was China.

Italy may be a Group of Seven country and NATO partner, but U.S. influence over this decision appears to have been limited. Italy has gone ahead on its own to welcome Chinese involvement in its economy.

With weak European enforcement of EU rules and transparency requirements, U.S. and European partners should continue to pressure Italy at every opportunity to seek full accountability and transparency for all the terms, as well as protections for sensitive technologies.

Both sides of the Atlantic should pressure Italy to avoid agreements that open dark holes of unknown commitments and that would undermine decades of improvements in financial stability and progress in adopting best practices by governments and businesses.

Meg Lundsager is a public policy fellow at the Wilson Center consulting on international economic, financial and regulatory issues. She is the former U.S. executive director at the International Monetary Fund.